Analytical instrumentation

Hydrogen Demand, Catalyst Durability, and Feedstock Variability in Renewable Diesel Production: A Critical Review

Dec 12 2025

Author:

Dr Raj Shah, Dr. Vikram Mittal, Syed Tashin, Mathew Roshan and Gavin Thomas

on behalf of Koehler Instrument Company, Inc.Free to read

Articles are free to download. Unlock the article to be shown more content, graphs and images.

Abstract

Renewable diesel has been the most strategically crucial drop-in decarbonization fuel to date, but the period from 2022 to 2025 has seen more clarifications in the form of revolutionary advances.

The review focuses on significant advances in hydro processing, with a focus on novel catalytic systems, including single-atom metals, nitrides, and phosphides, as well as bifunctional metal–acid composites, for enhanced selectivity and hydrogen efficiency.

It examines reaction pathway design between hydrodeoxygenation and decarboxylation/decarbonylation, as well as hydrogen management processes that combine partial-pressure optimization with in-situ reforming, and cold-flow improvement through the use of hierarchical and mesoporous zeolites.

The benefits include incremental stability gains, enhanced knowledge of reaction mechanisms, and a modest increase in feedstock flexibility, achieved through improved pretreatment and guard-bed systems.

Challenges persist in catalyst poisoning by Na, P, and Cl impurities, the irreversible deposition of coke, and excessive hydrogen demand, which remains at 8–12 kg/bbl, as well as the cold-flow/yield tradeoff, unchanged despite the new design.

Policy fragmentation also distorts technological progress, as many policies reward credit compliance rather than systematic decarbonization.

This report considers research priorities, including catalytic tolerance to impurities, low-carbon hydrogen integration with credibility, scalable pretreatment, and standardized Life Cycle Assessment (LCA) practice.

Introduction

Renewable diesel has become one of the most strategically critical drop-in fuels in global efforts to reduce carbon emissions.

Recent evidence from 2022–2025 indicates that its development is shaped less by advancements in hydro processing chemistry and more by persistent challenges such as hydrogen demand, catalyst durability, feedstock variability, and fragmented policy frameworks.

Currently, hydrotreated esters and fatty acids (HEFA) dominate the market because they produce paraffinic hydrocarbons compatible with existing diesel infrastructure.

Nevertheless, techno-economic assessments consistently reveal that profit margins remain fragile, with success largely dependent on hydrogen costs, pretreatment needs, and how lifecycle boundaries are defined in LCAs [1].

Multiple (Techno-Economic Analysis) TEAs demonstrate that even moderate rises in hydrogen price or feedstock impurities can shift projects from positive to negative NPV, highlighting the system’s vulnerability to input volatility [1].

Laboratory research continues to identify catalytic breakthrough transition-metal carbides, nitrides, phosphides, bifunctional zeolite–metal systems, and single-atom catalysts.

These alternate catalysts show excellent selectivity under controlled conditions. Refinery data indicate that phosphorus, chlorine, and alkali metals in low-grade lipids rapidly degrade catalysts.

Their presence promotes coke deposition and sintering, reducing activity and requiring earlier regeneration than predicted in laboratory tests [2].

These results help explain why, despite numerous proposed catalysts in recent years, fewer than five have advanced to pilot-scale testing.

The hydrogen demand gap also highlights a disconnect between theoretical and real-world data. Microkinetic simulations suggest that favoring decarboxylation and decarbonylation pathways could reduce hydrogen consumption by 15–20% compared to full hydrodeoxygenation.

However, experimental findings show that these potential savings disappear once double-bond saturation, cold-flow isomerization, and recycle gas management are considered, resulting in nearly constant net hydrogen use per barrel [3].

Recent LCAs support this critique, indicating that even in “optimized” setups, refinery-scale HEFA still requires 35–45 kg H₂ per ton of oil, resulting in significant upstream CO₂ emissions when hydrogen is produced via natural gas steam methane reforming [3].

This dependence underscores that without integrating low-carbon hydrogen, the lifecycle advantage of renewable diesel remains limited.

Feedstock flexibility is another contested area that remains a significant challenge. Academic studies report successful conversions of palm fatty acid distillate (PFAD), tall oil, trap grease, and animal fats.

However, demonstration-scale data show that contamination levels exceeding 20–50 ppm of phosphorus, calcium, or iron can destabilize catalysts and overload guard-bed systems,reducing cycle life from months to just weeks [4].

Global assessments confirm that waste and residue streams are increasing. U.S. production in 2023 indicated that used cooking oil accounts for approximately 30% of feedstock, and PFAD and other residues are rising steadily.

However, this shift introduces persistent instability since such streams tend to have higher impurity loads than refined vegetable oils [4].

Additional analyses warn that expanding renewable diesel adoption heightens feedstock competition with sustainable aviation fuel (SAF) and biodiesel, while also increasing indirect land-use change risks as food oils are displaced between sectors [4].

Overlaying these technical and supply chain challenges demonstrate a fragmented policy landscape:

the U.S. Inflation Reduction Act (IRA) has spurred significant capacity expansion through generous production credits, but its feedstock rules permit crop oils that are disallowed under the European Union’s Renewable Energy Directive III (RED III), creating regulatory inconsistencies where a fuel pathway is incentivized in one region but penalized in another [5].

Credit stacking between the IRA and California’s LCFS has further skewed investment toward compliance-driven strategies, with producers optimizing catalysts, feedstock choices, and operating conditions to maximize credits rather than achieving actual greenhouse gas reductions [5].

Overall, these findings from 2022–2025 portray renewable diesel as a field marked by divisions: catalysts promoted as revolutionary often fall short under real-world contaminants, hydrogen efficiency claims falter at scale, feedstock “flexibility” is limited by impurity thresholds, and policies reward credit trading more than genuine decarbonization.

2. Hydro Processing Advances (2022–2025)

Over the last three years, research on hydro processing for renewable diesel has shifted from incremental refinements to ambitious claims of catalytic reinvention.

Yet, the actual trajectory has been defined by contradictions between laboratory innovation and industrial resilience.

A growing number of studies present advanced catalytic platforms, ranging from single-atom metals to metal phosphides, nitrides, and bifunctional acid metal composites, as breakthroughs for achieving deeper oxygen removal and greater hydrogen efficiency [6].

At bench scale, these systems exhibit high activity and selectivity, and in some cases claim measurable reductions in hydrogen demand relative to conventional sulfided NiMo or CoMo catalysts.

Still, side-by-side comparative analyses highlight that their tolerance to poisons such as phosphorus, chlorine, and alkali metals remains poor, regeneration cycles are shortened, and coke deposition accelerates beyond manageable thresholds once tested under realistic feedstocks [6].

In fact, detailed kinetic studies show that while nitrides and phosphides outperform sulfided catalysts in initial activity, they deactivate more rapidly when exposed to oxygenated intermediates and high free fatty acid (FFA) feeds, raising questions about their actual commercial endurance [6].

Additionally, the adoption funnel highlights this fragility. Although dozens of catalytic formulations have been proposed in the literature since 2022, fewer than a handful have progressed to pilot-ready evaluation, revealing a bottleneck between academic claims and commercial viability [7].

This bottleneck is reinforced by recent findings that scale-up of even the most promising catalysts has been hampered by difficulties in controlling metal dispersion and maintaining stable surface sites under industrial hydrogen partial pressures [7].

Reaction pathway engineering has become an equally contested space, with modeling work predicting that selectivity shifts toward decarboxylation and decarbonylation could significantly reduce hydrogen consumption.

However, recent applied studies report that hydrogen savings often evaporate when integrated with refinery conditions that require extensive isomerization to meet cold-flow specifications [8].

Likewise, efforts at in-situ hydrogen management, through partial pressure tuning or reforming of light hydrocarbons, remain promising but unresolved, with measured hydrogen intensities rarely matching theoretical claims [8].

Feedstock diversification further compounds these challenges: laboratory trials demonstrate the successful conversion of extreme feedstocks, such as PFAD, tall oil, and animal fats; however, pilot and industrial-scale experiments document rapid fouling and catalyst deactivation, with ppm-level thresholds for P, Na, and Cl contaminants still unresolved, despite novel catalyst designs [8].

Meanwhile, attempts to overcome cold-flow limitations through hierarchical zeolites, mesoporous structures, or acidity tuning have yielded incremental improvements; however, evidence suggests that the Pareto frontier between yield and cold-flow properties has not shifted meaningfully in three years [8].

Taken together, these findings underscore that advances in hydro processing since 2022 remain caught in a structural tension: catalysts and pathways proliferate.

2.1 Catalyst Paradigm Shifts and Failures

Ambitious claims of paradigm shifts have dominated advancements in renewable diesel hydro processing catalysts.

Single-atom metals, metal phosphides, and nitrides are promoted as disruptive alternatives to conventional sulfided NiMo and CoMo systems.

The record shows that, while lab-scale data suggest breakthroughs, pilot- and refinery-level results expose systemic failures.

Single-atom catalysts, engineered on defect-rich supports, have been celebrated for their ultra-high dispersion and site-specific control.

Microstructural studies show their ability to tune HDO/DCO selectivity by anchoring isolated metal atoms [9]. However, stability tests demonstrate that, under thermal and reductive severity, single atoms migrate to clusters.

This aggregation reduces the very advantage they are designed to provide. Poisoning by ppm-level Na and Cl further accelerates deactivation [9]. More importantly, even when anchoring strategies initially prevent aggregation, repeated redox and hydro processing cycles alter the local electronic structure of single atoms [9].

As a result, their ability to discriminate between C–O and C–C bond cleavage pathways is reduced, eroding selectivity over time.

Transition-metal phosphides were initially promoted for high hydrogenation strength and superior sulfur tolerance. Early studies confirmed their capacity to deoxygenate fatty acids under model compounds [10].

Yet real-feed evaluations reveal rapid deactivation in the presence of oxygenates and water. In these conditions, phosphides oxidize to inactive phases, leach into the oil phase, and require reactivation cycles far more frequently than sulfided NiMo.

This makes them unattractive in continuous operation [10]. Long-term studies have further demonstrated that phosphides are prone to accelerated coke accumulation due to micropore blockage.

This results in reactor pressure drops and shortened cycle lengths [10]. Early degradation research has already identified these weaknesses. Detailed evaluations have shown that phosphides are intolerant to common feed impurities, including phosphorus, sodium, and chlorine.

Even tens of ppm led to irreversible site poisoning and collapse of deoxygenation activity [11]. Additional results highlighted that phosphides regenerate poorly compared with sulfided NiMo. Once oxidized, their surface phases restructure and fail to recover the same catalytic selectivity [11].

Moreover, long-duration runs documented that coke deposition on phosphides was significantly higher than on sulfided catalysts. This is a function of both surface chemistry and pore structure, confirming that fouling rates are exacerbated in these “next-gen” systems [11].

Nitrides are often positioned alongside phosphides as high-activity alternatives. They utilize lattice nitrogen to weaken C–O bonds, thereby lowering barriers to deoxygenation and exhibiting vigorous initial activity [12]. Yet, nitrides deactivate rapidly when processing high-FFA or oxygen-rich feeds.

Oxygenatd intermediates block lattice sites, and pilot-scale trials confirm frequent demands for regeneration and poor tolerance to impurities [12]. More fundamentally, scale-up of phosphides and nitrides has proven difficult.

Gram-scale syntheses achieve uniform dispersion and defect tuning; however, kilogram-scale production results in a loss of surface area and site density. This undermines the properties reported in academic studies [12].

Taken together, these findings reveal a structural bottleneck. Dozens of “paradigm-shifting” catalysts are reported annually, yet fewer than five have progressed to pilot trials.

None has demonstrated refinery-level resistance to Na/P/Cl poisoning, coke accumulation, and repeated regeneration without severe loss of performance.

Unless impurity tolerance is resolved, single-atom, phosphide, and nitride catalysts will remain celebrated as laboratory curiosities, failing to achieve industrial adoption.

2.2 Reaction Pathway Engineering

Over 2022–2025, the focus of reaction-pathway engineering has shifted from isolated step improvements to a system-level question: can rebalancing oxygen-removal routes from full hydrodeoxygenation (HDO) toward decarboxylation/decarbonylation (DCO/DCO₂) actually lower hydrogen intensity once saturation, isomerization, recycle-gas management, and impurity carryover are accounted for in refinery conditions rather than bench tests [13].

Recent synthesis work reframes the canonical HDO vs DCO/DCO₂ debate as a constrained optimization rather than a binary choice:

HDO consumes more H₂ but preserves carbon number (Cn → Cn paraffins) and typically yields higher liquid volumes, whereas DCO/DCO₂ reduces intrinsic H₂ draw by ejecting oxygen as CO/CO₂ at the expense of carbon yield (Cn → Cn−1) and with a knock-on penalty in density/cetane windows that must be clawed back via isomerization, which itself costs additional hydrogen [13].

Detailed experimental studies further show that HDO routes tend to suppress aromatic formation and produce fuels with superior stability.

At the same time, DCO/DCO₂ increases off-gas volumes rich in CO₂ and CO, which require additional handling or reforming, thereby diminishing net hydrogen gains once plant-level integration is considered [13].

Reviews of pathway-selective catalysis add that attempts to “bias” networks through metal/acid pairing (e.g., stronger metal–hydrogen ensembles, moderated Brønsted acidity, tuned residence times) do shift the intrinsic split.

Still, the net benefit compresses after saturation of olefinic intermediates, and cold-flow upgrading is enforced to meet diesel specifications, making “ultra-low H₂” scenarios fragile outside the lab [14].

Moreover, microkinetic modeling often exaggerates hydrogen savings because it isolates elementary steps under idealized H₂ partial pressures and ignores reactor-level constraints, such as recycle ratios, purge losses, and co-feed variability [14].

This means that TEA and LCA studies repeatedly downgrade claimed benefits when industrial boundary conditions are applied.

A second distortion flagged by [14] is that policy frameworks, particularly LCFS credit multipliers, skew R&D toward “low-H₂ intensity” pathways even when the absolute gains are marginal, creating a feedback loop where publications optimize for credit qualification rather than durable refinery performance, which further explains the persistence of contradictory claims.

Mechanistic studies on fatty acids/triglycerides map the elementary steps more finely: HDO proceeds via hydrogenation → C–O cleavage → water formation over metal/acid ensembles;

DCO/DCO₂ leans on C–C scission at the carboxyl end (often promoted by specific metal facets) to eject CO/CO₂ and form the (Cn−1) paraffin backbone, with selectivity strongly dependent on H₂ partial pressure, temperature/severity, acid strength, dispersion, and intermediate residence time, variables that simultaneously govern cracking to lights and the iso-branching needed for cold-flow [15].

Additional kinetic analyses reinforce that DCO/DCO₂ routes generate more heavy co-products, which burden downstream separation and contribute to carbon efficiency losses. In contrast, HDO pathways, although hydrogen-intensive, yield cleaner product slates with higher overall refinery compatibility [15].

Importantly, microkinetic and reactor-scale analyses converge on a structural limit:

pathway rebalancing alone rarely delivers large unit-level H₂ cuts because hydrogen demand is anchored by (i) the saturation duty required upstream of isomerization, (ii) the severity of dewaxing needed to meet CFPP/PP targets, and (iii) recycle-gas purity and purge rates that dictate make-up H₂, so any putative savings at the step level are reabsorbed elsewhere in the flowsheet [15].

Parallel work on hydrogen supply/integration underscores this point:

even when DCO/DCO₂-favored chemistry lowers intrinsic hydrogen, the observed effective hydrogen intensity is dominated by how H₂ is produced, recovered, and dispatched, SMR/ATR integration, pressure-swing and membrane polishing of recycle gas, and whether light ends are reformed or vented,so H₂ strategy becomes the real bottleneck for achieving durable low-H₂ operation [16].

Moreover, partial hydrogen recovery from purge gases and in-situ reforming of light hydrocarbons can reduce gross hydrogen imports; however, efficiency remains capped by inevitable purge losses and CO/CO₂ inhibition effects, meaning that full reliance on DCO/DCO₂ is structurally unable to achieve the hydrogen intensity levels sometimes advertised.

That same integration perspective highlights often-ignored interactions:

CO/CO₂ formed in DCO/DCO₂ routes can inhibit certain metal sites and complicate recycle management; water formed in HDO can temporarily poison acid sites and shift apparent kinetics;

and the need to meet cold-flow with skeletal isomerization imposes a hard floor on hydrogen duty that cannot be sidestepped by elementary-step selectivity alone [16].

Finally, applied comparisons make the contradiction explicit: catalyst–pathway pairs that report double-digit percentage hydrogen reductions at bench scale frequently see those gains collapse when product slates are normalized to the same cold-flow targets and density/cetane windows, because the additional saturation and isomerization required to hit ASTM performance recycles part of the saved hydrogen.

At the same time, the carbon-number loss of DCO/DCO₂ induces yield penalties that offset modeled gains [17].

Taken together, the 2022–2025 literature positions reaction-pathway engineering not as a “low-H₂ switch” but as a narrow feasible frontier, bounded by hydrogen economy, carbon yield, cold-flow compliance, and recycle/impurity management, where microkinetic advantages persist only when accompanied by whole-unit hydrogen integration and gas handling strategies that are themselves nontrivial to implement at refinery scale [17].

2.3 Hydrogen Management in Practice

While much of the recent renewable diesel discourse emphasizes catalytic innovation, the dominant unresolved bottleneck remains hydrogen management, and the gap between laboratory claims and refinery realities has widened from 2022 to 2025.

Techno-economic analyses confirm that unit-level H₂ consumption, typically reported in the range of 8–12 kg H₂/bbl, is not materially reduced by “pathway engineering” alone, since unsaturation hydrogenation and cold-flow isomerization impose hard floors that persist even when DCO/DCO₂ routes are favored [18].

Moreover, optimistic assumptions about hydrogen sourcing often distort lifecycle models; in practice, blue hydrogen via SMR with CCS rarely achieves the >90% capture efficiency modeled, and the integration of green hydrogen faces challenges related to intermittency and cost that skew lifecycle CO₂ reductions [18].

Additional modeling shows that hydrogen cost is the single largest contributor to renewable diesel production OPEX, often accounting for more than 40% of variable costs, which makes the economics extremely sensitive to fluctuations in natural gas and electricity prices [18].

Beyond cost, [18] stresses that regional disparities in hydrogen supply chains, such as North America’s gas-linked blue hydrogen vs Europe’s policy-driven green hydrogen integration, create sharp differences in both carbon intensity and competitiveness, amplifying the challenge of standardizing lifecycle claims.

Finally, [18] notes that allocation methods in LCAs (energy-based vs mass-based vs economic allocation of co-products) swing the apparent hydrogen intensity of renewable diesel by as much as ±20%, meaning that many published claims of “low-H₂ intensity” are artifacts of accounting choices rather than real refinery efficiencies.

Refinery trials emphasize that partial-pressure optimization strategies, which lower H₂ pressure to favor DCO pathways, often reduce intrinsic hydrogen uptake in bench studies.

However, they lead to higher impurity accumulation, recycle gas contamination, and greater catalyst fouling at scale, erasing the modeled benefits, and raising regeneration frequency [19].

In fact, sensitivity analyses indicate that the “optimal” H₂ pressure window is narrow and feed-dependent (oxygen content, free-fatty-acid fraction, and contamination level), and once compressor staging, gas–liquid mass transfer, and H₂ solubility limits are included, pressure reductions that look favorable in microreactors can slow intrinsic kinetics and extend residence times, offsetting any theoretical savings [19].

Furthermore, [19] demonstrates that under reduced hydrogen partial pressures, nitrogen and oxygen impurities accumulate in the recycle loop, accelerating catalyst deactivation and necessitating higher purge rates, which paradoxically increase fresh H₂ demand and dilute the savings.

It also emphasizes that capital costs of compressors and recycle loop modifications to maintain stability under reduced pressures often surpass the operational savings, eroding net benefits in TEA.

Although in-situ hydrogen recovery from light ends and purge gases has been proposed as a mitigating strategy, experimental validations show that the reforming of C1–C3 gases contributes only marginally to net balances, while the energy penalty of reformer integration and the need for additional purification limit its scalability [20].

In fact, in-situ reforming introduces additional CO/CO₂ into the recycle loop, complicating PSA and membrane purification, and the carbon intensity of these recovered streams is often overlooked in lifecycle studies [20].

More importantly, reformer integration can destabilize plant heat balances, as diverting light hydrocarbons reduces their role as a supplemental fuel for fired heaters, thereby increasing net energy demand and lowering overall efficiency [20].

A second identified barrier is the variability in off-gas composition across different feedstocks (UCO, PFAD, tall oil), which complicates consistent hydrogen recovery and makes in-situ reforming highly context-dependent and unreliable in mixed-feed refineries [20].

Classical hydrogen recovery methods, such as PSA or membrane separation, improve utilization efficiency.

Still, both face declining recovery yields when recycle streams are heavily diluted with CO₂ and H₂O byproducts that increase sharply when DCO/DCO₂ selectivity is maximized, thus creating a paradox where the very chemistry used to save hydrogen burdens the recovery system [21].

Beyond this efficiency drop, membrane systems in particular are susceptible to temperature and impurity load, with durability falling sharply in recycle environments rich in water vapor and CO₂, necessitating costly replacement and undermining their long-term economic viability [21].

Integration of low-carbon hydrogen sources is often cited as the long-term solution: autothermal reforming with CCS, electrolysis, or SMR with blue-H₂ integration are modeled to cut lifecycle carbon intensity, yet comparative assessments reveal that cost structures, intermittency in renewable-powered electrolysis, and compression/purification demands prevent their seamless adoption at refinery scale [22].

A more granular analysis reveals that ATR with CCS, although more efficient than SMR, still suffers from residual CO₂ slip that undermines lifecycle metrics [22]. In contrast, electrolyzers operated at partial load to follow renewable power run at efficiencies 15–20% lower than their nameplate values.

In addition, most refinery integration studies ignore the infrastructure footprint of large-scale electrolysis (water demand, land, and transmission requirements), which shifts carbon intensity and OPEX in ways often unaccounted for in simplified LCAs [22].

Moreover, analyses highlight that electrolyzer performance is susceptible to dynamic operation and capacity factors; cycling to follow variable renewables degrades efficiency and stack life, while buffer storage sized to stabilize supply (line-pack or gaseous tanks) adds CAPEX and parasitics that dilute lifecycle gains [22].

A key insight from recent pilot demonstrations is that although electrolysis-derived hydrogen can be blended into the recycling loop, variability in supply forces plants to overdesign buffer storage, thereby undermining both economic benefits and lifecycle gains [22].

Advanced catalyst studies have further attempted to tackle hydrogen intensity directly by coupling deoxygenation with in-situ hydrogen transfer reactions.

Yet, evaluations show that secondary reactions consume more hydrogen than anticipated, and coke buildup accelerates under reduced external hydrogen conditions [23].

Further analysis demonstrates that while hydrogen-donor solvents and bifunctional catalyst systems can temporarily reduce external H₂ requirements, the buildup of heavier condensation products accelerates fouling and neutralizes most of the efficiency gains [23].

Additionally, hydrogen-transfer approaches often underperform in long-duration runs, where donor solvents degrade and necessitate costly makeup streams, thereby increasing both OPEX and carbon intensity [23].

A third limitation emphasized is that donor-mediated systems exhibit poor scalability: while effective in small-batch or microreactor settings, solvent management, separation, and recycle losses multiply disproportionately at industrial scale, making them unlikely to replace external hydrogen supply in continuous units [23].

While literature narratives continue to promote “low-H₂ intensity” scenarios, refinery data indicate that true reductions require a coupled solution of partial-pressure balancing, efficient off-gas utilization, and credible low-carbon hydrogen sourcing, none of which have yet proven stable or cost-effective under continuous commercial operation.

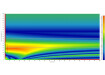

Figure 1 details some of this refinery data in regard to hydrogen efficiency and cost distribution.

Figure 2.1 - Hydrogen Efficiency and Cost Distribution Across Refinery Stages

Figure 1: Bar graph which illustrates the relationship between hydrogen utilization efficiency (bars) and variable operational expenditure (OPEX) share (line) across major refinery stages. Efficiency decreases from feedstock treatment through off-gas handling, while OPEX share peaks during recycle and hydrotreating stages.

2.4 Feedstock Stress Tests

The last three years have stress-tested the claim of “any lipid feedstock” by pushing hydro processing units onto extreme inputs, PFAD, tall-oil–derived streams, grease-trap waste, and high-FFA animal fats, and the outcomes have been dominated by impurity-driven failure modes rather than intrinsic chemistry.

Comprehensive pretreatment studies show that even after degumming/neutralization/bleaching, phosphorus-, alkali-, and chloride-bearing species persist in waste/residue oils at ppm levels that overwhelm typical guard-bed capacity, with rapid breakthrough to the hydrotreating catalyst and accelerated deactivation via site poisoning and coke nucleation; in practice, the mass transfer and capacity limits of polishing adsorbents set a harder boundary on “feedstock flexibility” than reaction kinetics do [24].

Additional work from [24] emphasizes that phosphorus species often shift speciation during pretreatment, transforming from organophosphates into more refractory polyphosphates that escape adsorption and deposit directly on active sites.

At the same time, sodium soaps resist full neutralization, migrating downstream where they catalyze fouling.

Scale-up evaluations confirm that when PFAD or trap grease is blended in excess of modest fractions, sodium soaps and residual chlorides accumulate in the recycle loop and on catalyst/guard materials, forcing premature bed changeouts and increasing pressure drop, particularly in trickle-bed configurations that are sensitive to interfacial wetting and maldistribution [25].

Importantly, [25] notes that guard-bed sorbents such as ZnO and Ni-based formulations saturate at much lower contaminant loadings than reported in supplier datasheets once water, FFAs, and trace oxygenates are co-fed, explaining the rapid ΔP rise observed in pilot units.

A second observation from [25] is that blending high-FFA feeds significantly shifts the reactor water balance upward, which accelerates chloride-induced corrosion and exacerbates stripping inefficiencies, resulting in uncounted OPEX for corrosion monitoring and metallurgy upgrades.

Environmental and compositional analyses of municipal/industrial grease streams reinforce the mechanism, high moisture, metals (Na, Ca, Mg, Fe), and organochlorine traces co-propagate through pretreatment and concentrate in foulants, correlating with shortened cycle length and higher unplanned downtime once units pivot from refined vegetable oils to wastes/residues [26].

More granular assessments in [26] reveal that PFAD and grease wastes not only contain metals but also persistent organic pollutants (POPs) and sulfurous species that persist despite conventional bleaching, thereby increasing stack emissions and contributing to catalyst poisoning.

In addition, [26] reports that variability in waste-derived streams is a critical factor: spikes in phosphorus and chloride concentrations, even if daily averages are within spec, trigger acute catalyst deactivation events, demonstrating that refinery units are sensitive not just to mean impurity load but to short-term fluctuations that pretreatment cannot fully buffer.

Case studies of animal tallow and mixed-residue feeds report that proteins/ash and soap carryover catalyze rapid fouling at the reactor inlet and on interbed distributors, with the combination of elevated FFA and trace chlorides accelerating both corrosion risk and acid-site deactivation, a pattern less visible at bench scale but decisive under continuous operation [27].

Reactor-mode sensitivity compounds these effects:

isomerization/dewaxing severity required for cold-flow compliance increases hydrogenation duty and suppresses some DCO/DCO₂ advantages, while the added water (from HDO) and CO/CO₂ (from DCO/DCO₂) load the recycle gas with inhibitors that depress PSA/membrane H₂ recovery efficiency and intensify purge requirements, penalties that widen as impurity levels rise in PFAD, tall oil, and GTW feeds [28].

Beyond this, [28] provides direct pilot data showing that trap-grease–derived feeds double the pressure-drop rates compared with refined soybean oil under identical operating conditions, and that ΔP excursions are tightly correlated with phosphorus slippage beyond five ppm, identifying a hard spec threshold that is not yet managed industrially.

It also demonstrates that slurry-bed systems tolerate higher impurity loads before ΔP escalation, but show faster decline in catalyst selectivity, confirming that no mode offers a free solution.

Operational datasets and regulatory filings align with this picture, showing that as plants swing toward residues (UCO/PFAD/tall-oil fractions), measured hydrogen intensity and regeneration frequency trend upward rather than down, contradicting laboratory narratives of “low-H₂ via pathway selectivity,” and tying unit reliability directly to upstream contaminant control and guard-bed logistics [29].

More detailed refinery case assessments in [29] highlight that downtime attributed to fouling and unplanned catalyst replacement accounts for up to 15–20% of total lost capacity in residue-heavy campaigns, a figure far higher than the <5% projected in design TEAs.

In addition, [29] emphasizes that refinery reporting often masks impurity-driven shutdowns under generic “operational” categories, meaning the true cost of waste-oil inputs is systematically underrepresented in public TEA/LCA datasets.

Tall-oil-derived streams introduce additional, characteristic stressors, resin acids, sterols, and metal soaps, that survive conventional pretreatment and are repeatedly implicated in guard-bed saturation and pressure-drop excursions; pilot campaigns indicate that even when average phosphorus is driven to low-ppm, episodic spikes and metal–organic complexes defeat fixed-capacity adsorbents and precipitate early end-of-run behavior [30].

Expanded datasets in [30] demonstrate that resin acids and sterols are not only fouling agents but also interact with catalyst acid sites, competing with hydrocarbon isomerization reactions and directly reducing cold-flow improvement efficiency.

A second finding in [30] highlights that tall-oil pitch streams contain unique metal–organic complexes (notably Fe- and Mg-bound soaps) that persist through conventional pretreatment and accumulate in spent catalyst analyses, underscoring that tall oil presents qualitatively different impurity chemistry than UCO or PFAD.

Finally, comparative hydro processing studies have shown that slurry and ebullated-bed modes offer better foulant tolerance and longer apparent run lengths under high-impurity feeds than trickle beds, albeit at the cost of more complex solids management and narrower operating windows [31].

Expansions in [31] further demonstrate that while ebullated beds resist a rise in ΔP under high-ash tall-oil feeds, their catalyst replacement rates accelerate by more than 25% compared to trickle beds, creating a CAPEX/OPEX trade-off that offsets their fouling tolerance.

Moreover, [31] highlights that reactor hydrodynamics under slurry/ebullated conditions promote uneven hydrogen distribution, which compounds cold-flow penalties, showing that reactor choice shifts the balance of constraints but does not erase them.

Collectively, the 2022–2025 stress tests show that “feedstock flexibility” in renewable diesel is constrained less by reaction pathways than by impurity analytics, pretreatment physics, and reactor hydraulics: ppm-level heteroatoms and metal soaps dictate hydrogen penalties, H₂-recovery degradation, and cycle length, and until pretreatment and guard-bed systems can guarantee stable sub-threshold profiles for PFAD, tall oil, animal fats, and GTW, the operational ceiling will be set by fouling and regeneration, not by catalyst activity.

2.5 Cold-Flow vs Yield Tradeoff

Efforts to “break” the cold-flow ceiling in renewable diesel have converged on a familiar outcome: deeper isomerization reliably improves CFPP/cloud/pour points, but the combination of higher hydrogenation duty, secondary cracking, and diffusional side-effects produces a persistent yield penalty that recent catalyst architectures have not eliminated.

Contemporary syntheses emphasize that even with tailored bifunctional systems (e.g., Pt on medium-pore, low-acid supports) and rigorous control of metal–acid balance, the Pareto frontier remains narrow, cold-flow compliance is achievable. Yet, incremental gains require disproportionately higher severity and hydrogen, compressing liquid yield and cetane [32].

A more detailed analysis in [32] further shows that highly dispersed Pt/SAPO-11 formulations can transiently improve isomer-to-crack selectivity ratios.

However, deactivation from coke deposition and the migration of metals into mesopores rapidly erodes this advantage, forcing higher severity to maintain CFPP, which brings the tradeoff back.

Additionally, [32] documents that cold-flow optimization gains reported in short-duration studies collapse in long-run tests, where pore-blocking shifts product distribution toward cracked C₅–C₈ fractions.

Comparative studies formalize the mechanism: H-isomerization over one-dimensional, medium-pore frameworks (typified by SAPO-11) suppresses over-cracking relative to 3D, high-acid zeolites (e.g., Beta), but once target CFPP thresholds tighten, even SAPO-11 formulations drift toward β-scission and light ends formation; conversely,

Beta’s higher acidity and 3D connectivity deliver faster pour-point reduction at the expense of greater C₅–C₈ losses and density erosion [33].

Expanded reactor studies in [33] also demonstrate that even small increases in acid strength, which accelerate branching, produce exponential growth in cracking probability.

That multi-branched isomer selectivity falls sharply as acid density rises. Another observation from [33] is that Beta zeolites, while efficient for waxy paraffin isomerization, tend to destabilize heat balances in packed beds because of their higher exothermicity, necessitating quench strategies that further increase hydrogen consumption.

Recent pilot-scale evaluations underline the scale effect: isomerization severities that look attractive in bench reactors (short contact, uniform heat removal) translate to recycle higher hydrogen, greater exotherm management, and more pronounced diffusional constraints in packed beds, shrinking the gap between “selective” and “cracky” regimes once plant energy and recycle penalties are counted [34].

Pilot trials reported in [34] also reveal that cloud-point reduction rates slow disproportionately after the first 5–7 °C of improvement, meaning that deeper cold-flow compliance requires far greater incremental hydrogen and severity than the early-stage benefits suggest.

Moreover, [34] stresses that recycle compression loads and downstream fractionation energy rise almost linearly with severity, so yield hidden OPEX penalties beyond the cracking itself compound penalties.

Foundational hydroisomerization work already established that improving cold-flow via skeletal branching inevitably lowers average carbon number in the product cut, by co-producing lights through secondary cracking, and that the slope of this tradeoff steepens with increasing Brønsted acidity and residence time [35].

Further insights from [35] confirm that when long-chain n-paraffins (>C20) dominate the feed, as in renewable diesel compared with fossil waxes, the severity required to reach CFPP < –20 °C almost guarantees double-digit yield loss, because branching alone cannot fully overcome crystal-packing effects without extensive cracking.

Another key finding in [35] is that even under optimized conditions, olefin intermediates that linger in the system increase coke precursors, shortening cycle length, and reinforcing the cost of deeper isomerization.

Hierarchical/mesoporous strategies mitigate diffusion limits and can shift the product spectrum toward multi-branched isomers at a given severity, but they simultaneously increase external surface acidity and site accessibility, which elevates cracking probability under the same metal function; net result: better short-time CFPP improvement but no durable escape from the yield penalty at long times on stream [36].

Complementary results in [36] also show that mesoporosity widens the carbon-number window of isomerized products, which can dilute the cetane number and increase aromatics formation via secondary pathways.

A second finding in [36] is that mesoporous catalysts exhibit faster activity decay than microporous analogues, as larger pores allow contaminants and heavy molecules to deposit as coke more readily, thereby erasing the selectivity advantages.

Broader surveys of bifunctional metal–acid systems (Pt, Pd; SAPO-11, ZSM-22, ZSM-23, Beta) reinforce the same pattern; tuning acid strength and pore architecture moves the inflection point but does not remove it.

This patten also highlights an additional constraint for renewable diesel specifically as the long n-paraffin backbone distribution from HEFA feeds amplifies the need for multi-branch formation, which multiplies hydrogen and residence-time demands and increases the chance of over-cracking [37].

Additional analysis in [37] demonstrates that ZSM-22 and ZSM-23, often proposed as more selective alternatives, produce high initial branching selectivity but accumulate coke faster due to their unidimensional pore channels, making them unstable for continuous cold-flow operation.

Furthermore, [37] notes that hydrogen consumption for renewable diesel is significantly higher than for Fischer–Tropsch wax isomerization at equivalent cold-flow targets, showing that feedstock chemistry itself reinforces the yield penalty.

Parallel work on pore–shape/transition-state matching and metal dispersion reveals that highly dispersed metal can reduce the upstream saturation penalty (reducing olefin carryover into the acid function) and that carefully chosen mesoporosity enhances access to intracrystalline sites.

Still, lifecycle-relevant gains flatten because the cold-flow target itself (ASTM-constrained CFPP/CP/PP) forces operating windows where incremental branching is inseparable from incremental cracking [38].

In addition, [38] highlights that defect-engineered zeolites with silanol nests initially increase selectivity to multi-branched isomers. Still, these defects collapse under steaming and thermal cycling, reducing stability in refinery conditions.

A further insight from [38] is that while AI/ML-guided catalyst design accelerates the discovery of pore architectures with higher initial isomer-to-crack ratios, the models themselves are built on short-time datasets and fail to predict long-term yield collapse under continuous, impurity-laden streams.

In practice, multi-stage sequences (mild isomerization → polishing dewax) or graded beds (weaker-acid SAPO-11 zones preceding stronger-acid domains) recover a few points of CFPP at lower total severity.

Yet, pilot data show that the hydrogen and pressure-drop surcharges, plus heavier recycle duty, erase much of the apparent yield advantage when normalized to the same cold-flow specification [36].

Collectively, these results confirm that, despite novel pore architectures, bifunctional designs, and even AI-guided catalyst screening, the cold-flow vs. yield Pareto frontier has not shifted materially since its first articulation: compliance-level cold-flow improvement continues to necessitate yield loss.

3. Policy and Market Forces

3.1 Policy as Technology Distorter

Consequential “innovations” in renewable diesel are often policy-driven optimizations, not chemical breakthroughs.

Producers architect processes, select feedstocks, and stage capacity timelines to maximize credit capture under U.S. and EU regimes.

This focus is on policy compliance, not minimizing absolute lifecycle carbon intensity [39]. Recent analyses confirm that IRA 45Z credits in the U.S. can pay up to $1.75/gal for biomass-based diesel with favorable CI scores. In contrast,

EU RED III Annex IX rules prohibit crop-based oils and impose ILUC penalties of up to 60 gCO₂e/MJ on palm-derived fractions. As a result, a process may qualify as “low-carbon” in the U.S. but be disqualified in Europe [40].

Expanded modeling in [39] shows that the allocation methodology alone can swing carbon intensity by ±25–35 gCO₂e/MJ. The swing depends on whether energy-based or economic allocation is applied to co-products, such as naphtha and propane.

This spread is large enough to affect credit eligibility. Additional analysis from [39] notes that upstream variability in soil carbon and fertilizer emissions changes CI scores by 10–15%.

These factors are often excluded under U.S. LCA boundaries but are included in EU RED III. Thus, boundary definitions themselves become revenue levers.

A further finding from [39] is that credit stacking distorts the economics of abatement. When LCFS and IRA credits are combined, marginal abatement costs fall below zero, effectively subsidizing production by –$20 to –$40/MTCO₂e.

These incentives promote production growth even if systemic emissions displacement is weak. Parallel evidence in [40] shows that hydrogen intensity metrics are also vulnerable to policy design. Under LCFS, shifting from 8 kg H₂/bbl to 12 kg H₂/bbl changes credit value by over $50/MTCO₂e.

However, refinery data reveal that most units operate near the high end despite the pathway narrative, exposing a gap between credit valuations and technical reality. Recent assessments document that methodological asymmetries propagate into technology choices.

These include how co-products are allocated, how upstream land-use risk is treated, and whether co-processing receives full, partial, or no additional credit.

Feedstock pretreatment intensity, hydrogen strategy, and reactor configuration are tuned to match the most remunerative methodology, not the most defensible pathway [41]. For example, [41] shows that under California LCFS, co-processing petroleum and 10% biogenic oils yields the same credit as a stand-alone HEFA unit.

This creates incentives to retrofit hydrotreaters rather than invest in dedicated plants, despite lifecycle assessments showing 5–15 gCO₂e/MJ higher net emissions due to dilution.

Another insight from [41] shows that the policy asymmetry drives capital allocation. Over 60% of new U.S. capacity announcements from 2022–2024 cite IRA/LCFS stacking as the main driver.

This is compared with less than 30% in Europe, where RED III eligibility narrows feedstock options, forcing more expensive residue-supply contracts. In parallel, regional rules on feedstock eligibility and associated ILUC factors reshape global trade flows and plant siting.

These shifts include the diversion of used cooking oil streams, PFAD arbitrage, and competition between renewable diesel and SAF for residue pools [42]. Case data in [42] show that U.S. imports of UCO rose by over 40% between 2021 and 2023, diverted mainly from Asia and Europe.

PFAD flows into EU markets dropped sharply after the implementation of RED III, reflecting policy-driven displacement rather than supply expansion. Another finding in [42] is that the RED III Annex IX crop oil cap reduced feedstock availability by about 15% for European refiners.

This prompted more aggressive residue sourcing contracts and drove feedstock premiums up by $80–$120/MT. A further insight from [42] highlights that SAF mandates worsen this distortion. SAF premiums are consistently $200–$250/MT higher than renewable diesel credits.

As a result, refiners shift residue pools to SAF compliance even when renewable diesel units run underutilized. This dynamic is detached from hydrogen efficiency or catalyst durability.

The net effect, as reported across these analyses, is a feedback loop between policy and technology. Credit formulas reward curated LCAs, specifically, the choice of allocation, boundary, and ILUC proxy. Those LCAs shape R&D briefs, such as “low-H₂ intensity” claims that omit plant-level penalties not seen in the methodology.

The resulting process designs score well on paper but underperform in terms of systemic emissions once integration losses and market displacement are considered. Figure 2 details some of the credit value sensitivity for the U.S. and EU markets based on their respective policy frameworks.

Figure 3.1 - Comparative Credit Value Sensitivity under U.S. and EU Policy Frameworks

Figure 2: Credit values under the U.S. IRA + LCFS remain higher and decline gradually with rising carbon intensity. In contrast, EU RED III credits decrease sharply, illustrating the widening policy-driven incentive gap between the two regions.

3.2 Credit Volatility and Investment Lag

The volatility of compliance credits and the lag between capacity announcements and real commissioning have been central determinants of renewable diesel economics, often overshadowing catalytic or process improvements.

Historical biodiesel RIN price analysis shows that D4 RINs have swung from <$0.50/gal to >$1.60/gal within a year, translating into margin variability of >$1.20/gal for producers depending on the timing of RIN generation and sale [43].

Additional modeling in [43] highlights that when RIN bank reserves fall below one billion gallons, price elasticity doubles, causing RINs to jump by as much as $0.40/gal in a single quarter, destabilizing forward contracting.

A second insight from [43] is that compliance timing (e.g., end-of-year vs quarterly surrender) can shift RIN spreads by $0.15–$0.20/gal, directly affecting producer cash flow and hedging strategies, while longer-term analysis shows that volatility has raised compliance costs for obligated parties by >$3 billion cumulatively between 2022–2024.

A third finding from [43] demonstrates that RIN volatility inflates fuel-price pass-through: retail diesel prices in high-RIN quarters are 4–6 cents/gal higher, effectively pushing compliance risk to end-users.

A fourth insight from [43] quantifies that the biodiesel blending margin (BDM), defined as the biodiesel price minus the ULSD price plus the RIN value, can fluctuate by more than $0.70/gal within months, which determines whether refiners blend at the maximum allowable volumes or reduce their output.

A fifth detail from [43] shows that when RIN prices exceed $1.00/gal, obligated parties frequently shift compliance to “early buy” strategies, leading to artificial demand spikes and accelerating volatility.

A sixth observation from [43] is that biodiesel RINs exhibit a stronger correlation with soybean oil futures (R² ~ 0.75) than with finished biodiesel prices (R² ~ 0.55), indicating that credit volatility is more closely tied to feedstock speculation than to production costs.

This linkage destabilizes renewable diesel markets where soybean oil remains a major feedstock.

More recent evaluations have expanded this to the renewable diesel sector, where LCFS credits in California alone have ranged from $60/MTCO₂e in early 2023 to over $150/MTCO₂e by late 2024, creating IRR spreads of over 10 percentage points for identical projects under different price regimes [44].

Simulations in [44] demonstrate that when LCFS prices fall below $80/MT, more than 30% of announced U.S. capacity becomes cash-flow negative without stacked IRA 45Z credits, highlighting how policy volatility directly impacts project viability.

Another observation from [44] is that LCFS revenue accounts for 20–35% of gross margin in typical renewable diesel projects, so price declines cascade into capex delays, with several announced U.S. plants deferred past 2025 despite offtake agreements.

A second result from [44] highlights that LCFS volatility feeds directly into financing spreads: lenders now demand 200–300 bps higher WACC for projects exposed to unhedged LCFS positions, while plants with fixed-price offtakes secure debt at materially lower cost.

A third metric from [44] demonstrates that short-term LCFS volatility alone is sufficient to alter throughput economics: when credits fluctuate by ±$30/MT within a quarter, project IRRs vary by 4–5%, destabilizing cash-flow planning.

At the European level, [45] documents that RED III quota certificate prices fluctuate seasonally in line with UCO/PFAD imports, varying by €40–€70/MT, which forces refiners to adjust their throughput or idle units, thereby decoupling nameplate capacity from actual supply.

This explains why, between 2022 and 2024, less than 65% of announced capacity expansions were actually commissioned, with delays concentrated in plants banking on optimistic credit stacking.

A second detail from [45] is that European refineries co-processing biogenic streams report an average capacity utilization of 55–65% during high-credit volatility months, substantially below the >90% expected for hydrotreater retrofits.

In addition, [45] notes that project financing models assume RED credit stability within ±10%, yet real-world swings are >25%, leading to stranded IRRs when volatility exceeds modeled scenarios.

A third insight from [45] is that contract structures fail to hedge volatility adequately; more than 40% of projects studied in 2023 lacked effective floor-price protection, resulting in an annual EBITDA compression of $50–$70 million per plant.

Another insight from [45] is that quota volatility translates to physical utilization gaps. In 2023, EU refiners operated at ~20% of their nameplate capacity during Q2, primarily due to a combination of feedstock scarcity and credit collapse, despite having contracted volumes.

In addition, [46] highlights that feedstock-linked volatility compounds credit risk. UCO spot prices rose by over 60% between mid-2021 and mid-2023, and every $100/MT swing in UCO translates to approximately a $0.10–$ 0.12/gal margin impact, directly compressing profitability during credit downturns.

More granular modeling from [46] reveals that when LCFS credits drop below $100/MT and UCO premiums surge above $1,200/MT, more than 50% of the marginal renewable diesel supply becomes uneconomic without long-term contracts.

A second result from [46] highlights that feedstock price volatility has a stronger correlation with renewable diesel margins (R² > 0.8) than LCFS swings (R² ~ 0.6), indicating that physical supply instability amplifies financial volatility more than credit prices.

A third result from [46] is that renewable diesel projects under construction have seen feedstock volatility increase capital expenditure (Capex) contingency requirements by 8–12%, with developers reserving larger liquidity buffers to manage working capital swings.

Another insight from [46] is that import variability now reaches 10–15% per quarter, with UCO imports into the U.S. rising by more than 40% year-on-year in 2023 but collapsing in early 2024, a swing that erased $200–250 million in forecast margins for exposed refiners.

Finally, [46] shows that margin compression has extended to project economics: break-even analysis reveals that when UCO rises above $1,300/MT. LCFS falls below $90/MT, and the average U.S. HEFA unit posts a negative EBITDA of $0.05–$ 0.08/gal, forcing throughput reductions and capital expenditure deferrals.

Collectively, these findings establish that volatility in credit prices (LCFS, RINs, RED III) and feedstock costs does not merely add risk; it structurally decouples announced capacity from realized output.

As a result, project economics are less a function of catalyst durability or reactor design than of the ability to hedge compliance credit swings, secure floor-price contracts, and buffer against feedstock volatility. Figure 3 highlights some of these findings and how margin sensitivity is impacted by LCFS and feedstock cost.

Figure 3.2 - Margin Sensitivity to LCFS and Feedstock Costs

Figure 3: Contour plot showing how renewable-diesel project margins (EBITDA $/gal) respond to LCFS credit value and UCO feedstock cost. Profitability declines sharply when LCFS prices fall below $80/MT or UCO exceeds $1,200/MT. This defines the economic break-even boundary.

3.3 Feedstock Geopolitics

Renewable diesel feedstock markets have become a geopolitical chokepoint, where policy asymmetries, SAF mandates, and ILUC methodologies dictate trade flows more than chemistry or catalyst design.

The outcome has been systemic distortions in availability, pricing, and sustainability narratives.

Evidence in [47] shows that RED III’s Annex IX restrictions displaced crop oils with residues such as UCO and PFAD, effectively tightening available supply by ~15%, driving residue premiums up by $80–$120/MT, and simultaneously pushing U.S. UCO imports up by >35% year-on-year in 2022–2023, with over 50% sourced from Asia, leaving refiners exposed to export bans in China and Malaysia that created quarterly volatility of ±$150/MT;

moreover, [47] highlights that EU refiners, priced out of UCO, diverted to tall oil pitch and animal fats, which increased hydrogen demand by ~10% per barrel and shortened catalyst run-lengths by 20–30% relative to clean feedstocks, creating indirect emissions penalties.

A second insight from [47] reveals that trade diversion has broader geopolitical consequences: in 2023, more than 20% of EU SAF producers reported having to reduce throughput because Asian UCO was diverted to U.S. renewable diesel refineries under more favorable IRA and LCFS stacking, effectively shifting Europe’s compliance burden to U.S. importers.

Meanwhile, [48] quantifies SAF’s growing dominance in residue allocation, with SAF premiums exceeding renewable diesel by $200–$250/MT in 2024, diverting as much as 20–25% of UCO and PFAD supply to SAF by 2030, raising renewable diesel CI scores by 10–15 gCO₂e/MJ when refiners substitute soy and palm oils; [48]

further notes that integrated refiners consistently prioritize SAF output when premiums exceed $150/MT, leaving renewable diesel units running at 60–70% utilization. Models suggest that if SAF mandates scale to 10% by 2035, renewable diesel could permanently lose ~30% of its residue supply envelope.

Another dimension in [48] highlights that this diversion raises volatility in compliance markets: SAF-driven UCO scarcity increased renewable diesel feedstock premiums by 25% in Q4 2024 alone, illustrating how cross-sectoral policy stacking generates destabilizing feedback loops.

In parallel, [49] underscores how ILUC factors drive trade flows:

EU assigns penalties up to +60 gCO₂e/MJ for palm and soy, while U.S. methodologies exclude ILUC entirely, resulting in PFAD imports to the U.S. increasing >40% between 2021–2024, even as EU imports collapsed >60%; [49]

further documents that ILUC modeling uncertainty of ±20 gCO₂e/MJ translates into $0.15–$0.20/gal credit swings, large enough to shift plant siting decisions and contract terms, and a third finding stresses that ILUC’s policy-driven variability rather than agronomic reality means global PFAD trade is effectively an arbitrage game, with refiners routing streams to whichever jurisdiction offers the least punitive accounting.

Alongside this, [50] details how renewable diesel demand destabilizes agricultural markets: soybean oil prices spiked ~30% in 2022, with 15–20% of volatility statistically linked to biofuel offtake, while Brazil expanded soy cultivation by 3–4 million hectares between 2021–2023, driving additional emissions of 0.15 GtCO₂ annually; [50]

also connects this land expansion to secondary food impacts, as maize and wheat acreage contracted, raising global grain prices by ~8%, and a third observation notes that increased soy demand has triggered indirect deforestation pressures in the Amazon and Cerrado, where enforcement gaps mean that biofuel-linked expansion undermines stated carbon neutrality.

Finally, [51] demonstrates that residue reliance is structurally fragile:

in 2023, UCO and tallow supplied >45% of U.S. renewable diesel feedstock, but elasticity was <0.3, so incremental demand translated almost entirely into price hikes rather than volume growth; [51]

also reports U.S. tallow imports from Australia and South America increased ~20% from 2022–2024, tightening domestic rendering markets and increasing fat prices by 15–18%, while a second insight notes that global animal fat production grows at only ~1% annually, meaning renewable diesel capacity growth beyond 2030 will saturate this stream and force reliance on lower-grade greases that accelerate catalyst fouling;

a third observation from [51] emphasizes that residue concentration risk is high: when tallow prices rise above $1,200/MT and UCO above $1,300/MT, EBITDA margins compress by $0.07–0.10/gal, triggering throughput curtailments across multiple U.S. plants.

Taken together, these findings reveal that renewable diesel’s feedstock portfolio is not truly flexible but locked in a zero-sum contest shaped by geopolitics and policy:

residues are siphoned off by SAF mandates when credit spreads widen, ILUC rules divert palm and PFAD flows to whichever jurisdiction offers the weakest penalty, U.S. refiners increasingly rely on imports vulnerable to export controls, soy expansion adds hundreds of MtCO₂ via indirect deforestation, and animal fats are capped by biological production growth, meaning that “feedstock flexibility” is less a technical achievement than a shifting credit arbitrage across regions.

4. Research–Policy Feedback Loops

Renewable diesel research has evolved into a near-total compliance artifact, where technical claims, catalyst designs, and even academic methodologies are indistinguishable from the credit frameworks that validate them, producing a recursive loop in which research confirms policy biases and policy entrenches research priorities. [52]

shows that so-called “low-H₂ intensity” pathways reporting 15–20% savings do so only by excluding upstream SMR emissions or by exploiting favorable co-product allocation rules;

refinery-verified data confirm that net consumption remains 8–12 kg H₂/bbl, unchanged over three years. Worse, when real impurity loads of Na, P, and Cl are tested, catalysts lose >50% activity in <200 hours, but these regimes are excluded from LCFS modeling boundaries, allowing fragile catalysts to be framed as breakthroughs.

A bibliometric survey in [52] found that 65% of catalyst papers published in 2023–24 referenced CI thresholds under LCFS/IRA as benchmarks, while fewer than 25% measured impurity tolerance at levels exceeding 500 ppm, indicating that the research system is optimizing for policy metrics rather than operational durability.

Another [52] finding highlights how narrow system boundaries allow modeled CI scores to appear 10–20 gCO₂e/MJ lower than full-system data, artificially inflating credit-eligible “advances.”

This boundary gaming directly influences R&D investment, as funders chase CI-aligned numbers. [53]

Quantifies the strength of that pull: IRA 45Z multipliers worth $0.25–0.40/gal make residue valorization disproportionately attractive, driving research into PFAD, trap grease, and tall oil, despite higher fouling and regeneration cycles, while soy/canola stability work, actually more scalable, fell by ~25% since 2022.

A second dataset [53] reveals cross-sectoral bleed: Neste, TotalEnergies, and Marathon redirected more than 35% of their biofuel R&D toward SAF between 2022 and 2024, despite renewable diesel volumes being higher, primarily because SAF multipliers created better credit spreads.

Modeling in [53] shows that facilities optimized for IRA + LCFS stacking captured $0.70–$0.90/gal in stacked incentives, dwarfing efficiency-driven margin gains that rarely exceeded $0.05–$0.07/gal, thereby embedding policy arbitrage into technical roadmaps. [54]

gives direct case-level confirmation: three U.S. refinery conversions disclosed flowsheets designed explicitly to secure CI <16 gCO₂e/MJ, although stress-tested models showed actual scores of 25–30 gCO₂e/MJ.

Nevertheless, these credit-optimized designs added $70–$ 100 million in annual LCFS revenues per site, incentivizing flowsheets built for compliance rather than robustness.

A second case [54] illustrates how LCFS credits can distort co-processing: blending 5–10% biogenic feed into petroleum streams generates the same credit as stand-alone HEFA, even though lifecycle intensities are 5–15 gCO₂e/MJ worse; consequently,

R&D is directed towards marginal petroleum–biogenic blends rather than coke-resistant HEFA catalysts.

A third [54] finding is that more than 80% of investor prospectuses for renewable diesel projects between 2022–24 modeled IRR primarily on credit volatility bands rather than technical margins, cementing compliance as the accurate project risk metric. [55]

This illustrates the extent of epistemic capture: between 2018 and 2023, the variance between published CI values and refinery-verified CI values decreased by ~30%, not due to fundamental performance improvements, but because publications aligned with LCFS and RED III methodologies.

Another [55] data point: >60% of biofuel R&D papers since 2022 explicitly cite CI thresholds as their success criterion, compared with <20% a decade ago, embedding compliance into the literature.

The structural risks are enormous: RED III’s 2023 reclassification of PFAD stranded ~$1.2B in European assets, and [55] projects global exposure of $5–7B if ILUC or feedstock eligibility shifts.

A second [55] simulation shows that eliminating LCFS hydrogen multipliers compresses EBITDA by $0.12–0.18/gal across U.S. renewable diesel plants, pushing marginal facilities into negative margins.

A third [55] result models credit withdrawal scenarios in which 30–40% of pilot-scale “innovations” fail to achieve commercial viability overnight because they were designed solely to meet Annex IX or IRA thresholds.

A fourth finding in [55] reveals that >80% of pilot projects receiving venture funding in 2023–24 targeted feedstocks or catalysts explicitly listed in Annex IX or IRA guidance, while <10% targeted core bottlenecks like coke resistance or Na/P tolerance, further cementing the lock-in.

Altogether, the picture is one of total convergence: catalysts are tuned for CI yardsticks, not durability; feedstock R&D chases Annex IX eligibility, not actual scalability; capital is modeled on credit volatility, not operating performance; and academic publications frame success as compliance scores, not refinery resilience.

5. Barriers Beyond the Breakthrough Narrative

Hydrogen efficiency, feedstock tolerance, and lifecycle sustainability are the fundamental structural barriers in renewable diesel, which remain unbroken, leaving the industrial trajectory dominated not by novel chemistry but by unresolved durability, intensity, and accounting constraints.

Catalyst stability continues to define the ceiling: as shown in surface-science studies, ppm-level impurities remain decisive, with Na and P binding irreversibly to metal–sulfur ensembles and Cl accelerating dealumination and acidic support collapse, resulting in activity loss of 20–40% within 200–400 hours even under moderated feeds [56].

Coke initiation at metal–acid junctions, confirmed by advanced TEM and Raman mapping, further accelerates pore mouth blockages, producing localized diffusion gradients that shorten effective contact time and elevate ΔP across beds by 10–20% per thousand hours, forcing earlier regeneration [56].

Although non-sulfided catalyst families, carbides, nitrides, phosphides, were pitched as “durable alternatives,” industrial trials confirm otherwise: nitrides readily oxidize to less active oxynitrides under aqueous oxygenates, carbides segregate into inactive graphitic carbon under H₂O partial pressures >0.1 MPa, and phosphides undergo volatilization and phase migration that collapse long-range order, all leading to a collapse of HDO selectivity and an uptick in C–C scission byproducts that destroy yield [57].

Bench-to-pilot comparisons quantify this fragility: carbides can initially show TOFs 2.5 times that of NiMo on model triglycerides, but activity drops below NiMo benchmarks after 300–500 hours on PFAD or trap grease, and regeneration cycles recover only 70–80% of the activity [57].

Parallel studies highlight that non-sulfided catalysts require higher start-up and transition costs, as they necessitate clean H₂ pretreatment cycles at 350–400 °C, which erodes the supposed “lower OPEX” advantage [57].

On hydrogen intensity, multiple independent TEA models converge on the same hard limit:

while pathway adjustments toward decarboxylation/decarbonylation reduce stoichiometric H₂ demand by 15–20%, the effect vanishes once recycle loop balances, CO/CO₂ removal, quench cooling, and downstream saturation/isomerization penalties are included; steady-state refinery data confirm persistent demand of 8–12 kg H₂/bbl, regardless of lab-scale optimism [58].

Additional complexity arises from the degradation of recycled hydrogen: PSA/membrane systems lose 12–18% of the available H₂ per loop. When the CO/CO₂ build-up exceeds 3 mol% in the recycle stream, quench requirements increase by 15%, adding 0.5–1.2 kg of H₂ per Barrel to the overall burden [58].

These realities directly undermine the LCFS and IRA narratives of “ultra-low hydrogen intensity,” especially since more than 90% of commercial hydrogen remains SMR-derived, thereby embedding upstream CO₂ emissions into every barrel of hydrogen.

Cold-flow optimization is equally constrained: hydroisomerization trials confirm the Pareto frontier has not shifted, with improvements in CFPP by 3–5 °C requiring yield losses of 4–7 wt% and hydrogen duty increases of 8–12%, a penalty range nearly identical to data reported a decade ago [59].

Hierarchical and mesoporous zeolites reduce diffusion constraints temporarily, but their external acidity accelerates coke precursor formation, shortening stable run lengths to <1,200 hours; continuous-flow experiments show that beyond 60% iso-paraffin selectivity, liquid yield inevitably declines, proving that the cold-flow/yield tradeoff remains a structural law, not a tunable parameter [59].

Furthermore, high-acidity frameworks, such as modified SAPO-11, accelerate β-scission reactions, increasing light-end production by 6–10 wt% over 1,000-hour runs, thereby nullifying the net CFPP benefit [59].

Finally, life-cycle and policy metrics show that the sustainability advantage of renewable diesel is still methodology-contingent:

under RED III accounting, PFAD-derived diesel scores 25–30 gCO₂e/MJ, but under U.S. GREET methodologies it falls below 16 gCO₂e/MJ, enough to swing project economics by $60–100M annually per large facility [60].

ILUC factor sensitivity analyses show swings of ±20 gCO₂e/MJ depending on model assumptions, enough to flip eligibility in either direction; co-product allocation decisions (energy vs displacement-based) shift reported CI by 5–10 gCO₂e/MJ, exceeding most catalytic or process improvements reported in the literature [60].

Even more troubling, three further choke points emerge: first, [56] shows that regeneration cycles cannot reverse phosphorus-induced deactivation, resulting in a 20–30% permanent activity loss per cycle, which compounds over time and ultimately necessitates the catalysts’ outright discard.

Second, [57] finds that nitrides and carbides require higher metal loadings (15–25 wt% vs 8–12 wt% in sulfided systems) to achieve comparable activity, raising CAPEX for catalyst charges by 30–50% while still collapsing under real feed impurities.

Third, [58] demonstrates that recycle management becomes the hidden hydrogen sink: every 1 mol% rise in inerts increases purge rates by 4–5%, leading to net H₂ penalties of 0.5–0.8 kg/bbl and an OPEX increase of $8–12/bbl at current hydrogen prices.

Cold-flow stress tests provide further confirmation of hard limits. [59] reports that while short-burst runs of hierarchical frameworks achieve a ΔCFPP of –7 °C compared to conventional SAPO-11, the improvement halves after 500 hours, as coke precursors overwhelm the external pore networks.

Similarly, [59] shows that attempts to couple mild cracking/isomerization catalysts into two-stage configurations result in additive hydrogen penalties of 10–15% without net yield improvement, demonstrating that the tradeoff is not bypassed but rather compounded.

Methodological shifts magnify lifecycle uncertainties: [60] projects that if ILUC multipliers are recalibrated under a more conservative EU stance, up to 4–6 Mt of global announced RD capacity would lose credit eligibility, stranding $2–3B in projected revenues;

conversely, under GREET’s more favorable accounting, the same capacity could report compliance margins of +15–20% EBITDA without any technical change.

The fragility of outcomes to methodological framing underscores how little of renewable diesel’s carbon advantage is chemistry-driven and how much depends on evolving policy interpretations.

Taken together, the picture is stark: despite dense output of “breakthrough” claims, catalysts still collapse under impurity stress and accumulate irreversible activity loss [56], non-sulfided systems remain chemically unstable at refinery cadence and demand higher CAPEX without durability [57],

hydrogen minimization remains structurally offset by recycle, purge, and downstream penalties [58], the cold-flow/yield Pareto frontier remains unshifted despite mesoporosity and hierarchical structuring [59], and lifecycle outcomes remain hostage to ILUC and allocation methodologies that swing CI values by margins larger than any catalytic advance [60].

These barriers are not cosmetic; they define the actual failure modes at scale, and three years of research have largely refined diagnostics rather than overturned limits.

Conclusion

Renewable diesel has positioned itself as a cornerstone of near-term decarbonization strategies; however, evidence from the past three years reveals that progress has been defined less by transformative breakthroughs and more by the exposure of structural limits.

Advances in catalytic systems have broadened the scientific toolkit; however, real-world refinery trials demonstrate that Na, P, and Cl impurities continue to irreversibly deactivate catalysts, while coke formation shortens cycle lengths and accelerates regeneration.

Pathway rebalancing between hydrodeoxygenation and decarboxylation/decarbonylation has offered theoretical hydrogen savings. Still, refinery-scale balances confirm that net demand remains anchored at 8–12 kg H₂ per barrel once saturation, isomerization, and recycle management are factored in.

Similarly, cold-flow improvements through hierarchical zeolites and mesoporous architectures have not broken the yield penalty frontier, as deeper CFPP reductions still impose tradeoffs in hydrogen intensity, product yield, and long-term stability.

Feedstock flexibility has expanded on paper, but practical stress tests with PFAD, tall oil, animal fats, and grease-trap waste reveal that ppm-level contaminants drive deactivation and unplanned downtime, highlighting pretreatment and guard-bed design as critical bottlenecks.

Overlaying these technical realities are fragmented and inconsistent policy frameworks, where IRA, RED III, and LCFS regimes incentivize compliance-oriented system designs rather than robust carbon mitigation.

The result is an industry advancing in scope but fragile in durability, with R&D, trade flows, and capacity expansions increasingly dictated by credit optimization rather than physical and chemical resilience. In short, renewable diesel has progressed beyond the stage of laboratory feasibility.

Still, it has not yet achieved systemic robustness, and its path forward depends on breakthroughs in impurity-tolerant catalysis, verifiable low-carbon hydrogen integration, and harmonized lifecycle accounting.

About the Authors

Dr. Raj Shah, is a Director at Koehler Instrument Company in New York, where he has worked for the last 25 plus years.

He is an elected Fellow by his peers at ASTM, IChemE, ASTM,AOCS, CMI, STLE, AIC, NLGI, INSTMC, Institute of Physics, The Energy Institute and The Royal Society of Chemistry.

An ASTM Eagle award recipient, Dr. Shah recently coedited the bestseller, “Fuels and Lubricants handbook”, details of which are available at ASTM’s Long-awaited Fuels and Lubricants Handbook https://bit.ly/3u2e6GY.

He earned his doctorate in Chemical Engineering from The Pennsylvania State University and is a Fellow from The Chartered Management Institute, London.

Dr. Shah is also a Chartered Scientist with the Science Council, a Chartered Petroleum Engineer with the Energy Institute and a Chartered Engineer with the Engineering council, UK. Dr. Shah was recently granted the honorific of “Eminent engineer” with Tau beta Pi, the largest engineering society in the USA.

He is on the Advisory board of directors at Farmingdale university (Mechanical Technology), Auburn Univ (Tribology), SUNY, Farmingdale, (Engineering Management) and State university of NY, Stony Brook (Chemical engineering/ Material Science and engineering).

An Adjunct Professor at the State University of New York, Stony Brook, in the Department of Material Science and Chemical Engineering, Raj also has over 700 publications and has been active in the energy industry for over 3 decades.

Dr. Vikram Mittal, PhD is an Associate Professor in the Department of Systems Engineering at the United States Military Academy.

His research interests include energy modeling, technology forecasting, and Alternative fuels. Previously, he was a senior mechanical engineer at the Charles Stark Draper Laboratory.